Working capital: What is it and why is it important?

June 3, 2026 | 6 minute read

Key takeaways:

- Working capital is the money a business has available to pay for current short-term obligations such as money owed to vendors and salaries of temporary employees.

- Two key measurements of working capital are working capital ratio and net working capital.

- Additional working capital may be needed to account for seasonal differences in cash flow and unexpected costs.

- Options to cover shortfalls in working capital include lines of credit and business credit cards.

Working capital — the money you have on hand to run day-to-day operations — affects many aspects of your business, from paying employees and vendors to planning for sustainable long-term growth. In short, working capital is the money available to meet your current, short-term obligations and is a terrific indication of a company’s health. Having enough working capital can make all the difference in building a business that’s thriving and ready to seek new opportunities.

To ensure you have the appropriate level of working capital to support your business and to be ready for the unexpected, you could calculate current working capital levels, project future needs and consider solutions to secure access to capital so you always have enough cash.

How to calculate working capital

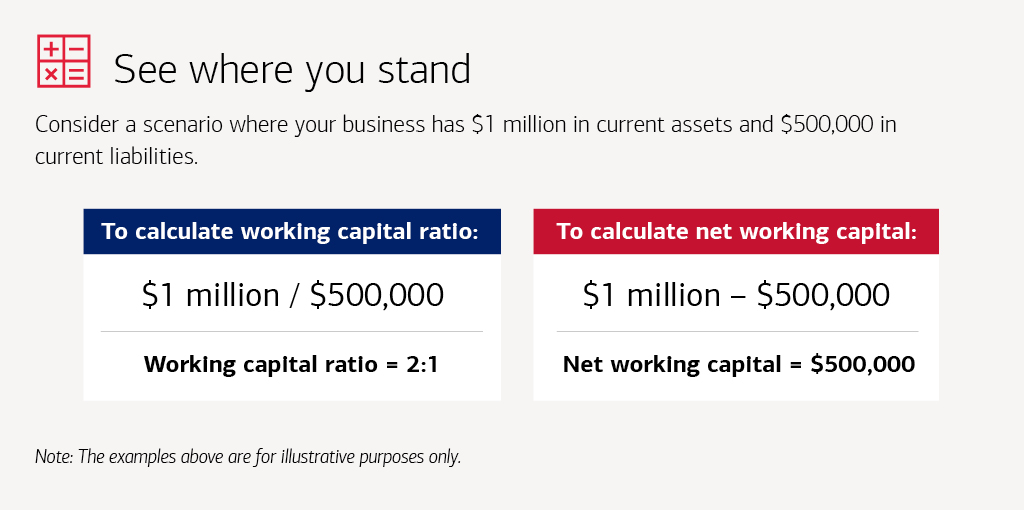

You can get a sense of where you stand by looking at two key measurements. Your working capital ratio (current assets divided by current liabilities) is a measurement of your company’s short-term financial health, and net working capital (current assets minus liabilities) tells you how much money you have readily available to meet current expenses.

A 2:1 working capital ratio, as in the example above, would generally be considered a healthy ratio, but in some industries or businesses, a ratio as low as 1.2 to 1 may be adequate.

For these calculations, consider only short-term assets and liabilities. Short-term assets, also known as current assets, include the cash in your business account and accounts receivable — the money your customers owe you — and the inventory you expect to convert to cash within 12 months. Short-term liabilities include accounts payable — money you owe vendors and other creditors — as well as other debts and accrued expenses for salary, taxes and other outlays.

Understanding your needs

Getting a true understanding of your working capital needs may involve plotting month-by-month inflows and outflows for your business. A landscaping company, for example, might find that its revenues spike in the spring, then cash flow is relatively steady through October before dropping almost to zero in late fall and winter. Yet on the other side of the ledger, the business may have many expenses that continue throughout the year. Working capital is the money you have available at any given time to pay your short-term obligations once your business liabilities are subtracted from its assets.

Forecasting your working capital needs could require making educated guesses about the future, something that could be challenging for some companies to do in an uncertain environment. While you can be guided by historical results, you’ll also need to factor in new contracts you expect to sign or the possible loss of important customers. It can be particularly challenging to make accurate projections if your company is growing rapidly.

These projections can help you identify months when you have more money going out than coming in, and when that cash flow gap is widest, so you can get a true picture of how much working capital you will have on hand.

Reasons why your business might require additional working capital

- Seasonal differences in cash flow are typical of many businesses that may need extra capital to gear up for a busy season or to keep the business operating when there’s less money coming in.

- Extra working capital can help improve your business in other ways. For example, it may enable you to take advantage of supplier discounts by using cash on hand to purchase in bulk. This can save you the interest you might have to pay using a credit card, which could be higher than for other types of credit.

- Working capital can also be used to pay temporary employees or to cover other project-related expenses.

- Working capital can help your business handle unexpected costs that arise in an uncertain environment.

Finding options to cover shortfalls in working capital

An unsecured, revolving line of credit can be an effective tool for augmenting your access to capital. Lines of credit are designed to finance temporary working capital needs. Lines of credit terms are generally more favorable than those for business credit cards. Your business can draw on the line of credit for capital whenever it’s needed and pay down the outstanding balance as business cash flow improves. A minimum payment is due each month.

While a business credit card can be a convenient way for you and top employees to cover incidental expenses for travel, entertainment and other needs, it’s usually not the best solution for working capital purposes. Drawbacks include higher interest rates, higher fees for cash advances and the ease of running up excessive debt.

Qualifying for a working capital line of credit

A working capital line of credit provides access to financing for short-term operating costs that are hard to predict, such as the need to purchase extra inventory during a sudden spike in demand. When you apply for a working capital line of credit, lenders will consider the overall health of your balance sheet, including your working capital ratio, net working capital, annual revenue and other factors.

Since small business owners’ business and personal finances tend to be closely intertwined, lenders may also examine your personal financial statements, credit score and tax returns. You may be asked for a personal guarantee of repayment. For a more detailed overview of what lenders look at, see “Factors that impact loan decisions (and how to increase your approval odds).”

Although many factors may affect the size of your working capital line of credit, a rule of thumb is that it shouldn’t exceed 10% of your company’s revenues.

Avoid working capital missteps

- Don’t confuse short-term working capital needs and longer-term, permanent requirements.

- While it can be tempting to use a working capital line of credit to purchase machinery or real estate or to hire permanent employees, these expenditures call for different kinds of financing. If you tie up your working capital line of credit on these expenses, it won’t be available for its intended purpose.

Your small business banker can help you better understand your working capital needs and what steps you might want to take to be prepared for any situation. While you can’t predict everything about running a company, a clear view of working capital can help you operate smoothly today — and set you up for long-term growth tomorrow.

Ready to meet with a specialist?

Our specialists are ready with advice and guidance to help move your business forward.

Cash flow management basics for small businesses

Maintaining a healthy cash flow can help ensure that you have cash available for your needs today and in the long term. But how do you do it?

The pros and cons of 5 financing options to help improve cash flow

Financing can be a useful tool to help you smooth cash flow. Know the pros and cons of various financing options so you can choose the best for your business.

Important Disclosures and Information

Bank of America, Merrill, their affiliates and advisors do not provide legal, tax or accounting advice. Consult your own legal and/or tax advisors before making any financial decisions. Any informational materials provided are for your discussion or review purposes only. The content on the Center for Business Empowerment (including, without limitations, third party and any Bank of America content) is provided “as is” and carries no express or implied warranties, or promise or guaranty of success. Bank of America does not warrant or guarantee the accuracy, reliability, completeness, usefulness, non-infringement of intellectual property rights, or quality of any content, regardless of who originates that content, and disclaims the same to the extent allowable by law. All third party trademarks, service marks, trade names and logos referenced in this material are the property of their respective owners. Bank of America does not deliver and is not responsible for the products, services or performance of any third party.

Not all materials on the Center for Business Empowerment will be available in Spanish.

Certain links may direct you away from Bank of America to unaffiliated sites. Bank of America has not been involved in the preparation of the content supplied at unaffiliated sites and does not guarantee or assume any responsibility for their content. When you visit these sites, you are agreeing to all of their terms of use, including their privacy and security policies.

Credit cards, credit lines and loans are subject to credit approval and creditworthiness. Some restrictions may apply.

Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as “MLPF&S” or “Merrill”) makes available certain investment products sponsored, managed, distributed or provided by companies that are affiliates of Bank of America Corporation (“BofA Corp.”). MLPF&S is a registered broker-dealer, registered investment adviser, Member SIPC, and a wholly owned subsidiary of BofA Corp.

Banking products are provided by Bank of America, N.A., and affiliated banks, Members FDIC, and wholly owned subsidiaries of BofA Corp.

“Bank of America” and “BofA Securities” are the marketing names used by the Global Banking and Global Markets division of Bank of America Corporation. Lending, derivatives, other commercial banking activities, and trading in certain financial instruments are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., Member FDIC. Trading in securities and financial instruments, and strategic advisory, and other investment banking activities, are performed globally by investment banking affiliates of Bank of America Corporation (“Investment Banking Affiliates”), including, in the United States, BofA Securities, Inc., which is a registered broker-dealer and Member of SIPC, and, in other jurisdictions, by locally registered entities. BofA Securities, Inc. is a registered futures commission merchant with the CFTC and a member of the NFA.

Investment products: