On this page

Economic and market brief

Monthly economic and market insights for business leaders

June 24, 2026

A turbulent year for business: What comes next?

An unexpected geopolitical conflict and persistent U.S. inflation have made 2026 unpredictable for business owners.

The focus now is what’s next and how leaders should respond.

In this 2026 Midyear Outlook webcast, Chris Hyzy of Merrill and Bank of America Private Bank’s Chief Investment Office examines the forces shaping the second half of the year, including supply chain disruption, cost pressures and accelerating technology change.

Explore the full 2026 Midyear Outlook to learn more about geopolitical risk, inflation’s impact on operations, AI’s role in productivity and how policy shifts may influence business planning.

Connect with a Bank of America business specialist to see how today’s economic changes could shape your strategy, costs and next phase of growth.

June 22, 2026

Making sense of economic trends for business planning

In this conversation, Sharon Miller, President of Business Banking at Bank of America, and Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank, connect the economic backdrop to real-world decisions facing business owners.

They discuss the current environment, including inflation, interest rates and credit conditions, along with business confidence, innovation and a preview of the 2026 Midyear Outlook.

For many owners, the challenge is translating economic headlines into business strategy and day-to-day decisions. Activity remains steady in many sectors, yet uncertainty continues to shape planning decisions.

The discussion highlights that market growth persists, but it is uneven. Businesses are navigating multiple forces at once, from policy shifts to global dynamics and evolving consumer behavior.

In a volatile economy, business owners should stay focused on flexibility, capital discipline and identifying where demand remains resilient. Connect with a Bank of America business specialist to align today’s economic insights with your capital, financing and growth decisions.

June 12, 2026

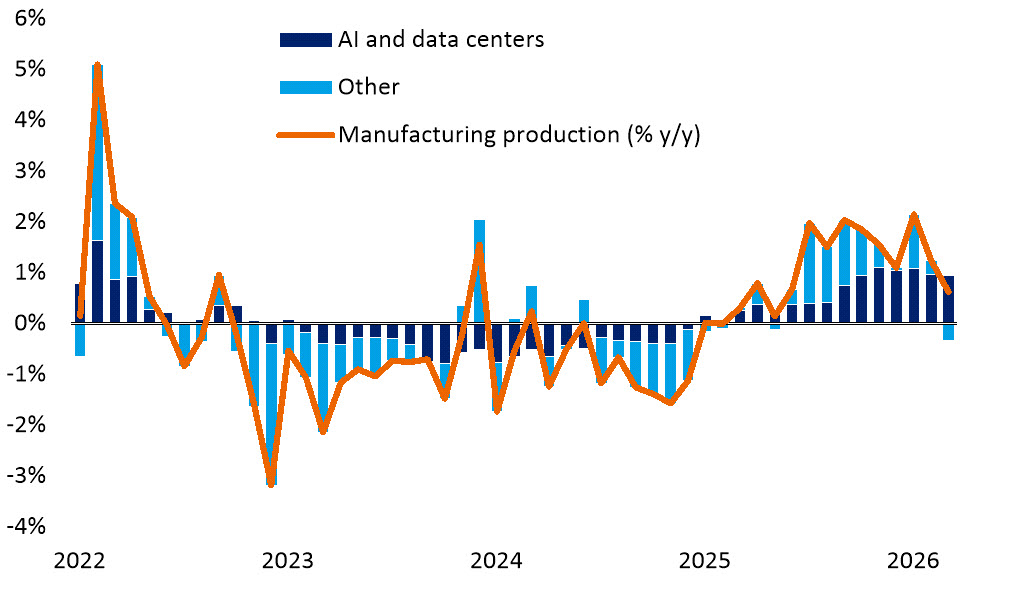

AI lifts manufacturing as investment fuels growth

Artificial intelligence is becoming a practical growth lever for business owners, especially in manufacturing. BofA Global Research expects U.S. GDP to grow 2.4% in 2026, with AI adoption helping boost productivity, support capital investment decisions, and strengthen overall economic momentum.

What Matters Today: Manufacturing production has been lifted by AI investment

Contributions to annual growth in manufacturing production

For business owners, the opportunity lies in “physical AI,” the integration of AI into robotics and industrial systems. Bank of America Institute highlights that humanoid and advanced robots could scale significantly, with the global population projected to reach 3 billion units by 2060. Early deployment is concentrated in manufacturing, where automation can help address labor shortages, rising wages, and operational inefficiencies while increasing output and consistency.

AI is also expanding beyond isolated tasks into connected systems. The technology is advancing toward a structural shift where “anything that moves is becoming autonomous,” spanning vehicles, industrial equipment, and logistics networks, while also unlocking multi‑billion‑dollar addressable markets across these sectors. For business owners, this signals a future where production, inventory, and distribution are increasingly integrated, enabling more efficient, scalable, and adaptive operations.

The implications are clear. Business owners investing in AI-enabled equipment and systems can help reduce costs, improve throughput, and strengthen resilience in a more complex operating environment. While upfront capital spending may increase, the payoff comes through higher productivity, better scalability, and stronger competitiveness.

April 17, 2026

Labor market steady amid uneven business demand

The Bank of America Institute finds the labor market that regained its footing in March, with payroll growth at 1.4% year over year. For business owners, that signals demand is holding up and hiring conditions are stabilizing after a choppy start to 2026. But growth is increasingly concentrated, which makes revenue visibility less predictable.

Wages tell the more important story. Higher-income households are seeing 5.6% growth, compared to 2.0% for middle-income and 1.0% for lower-income workers, the widest gap since 2015. That divergence is already reshaping spending. Premium demand is holding, while more price-sensitive customers are under pressure.

The driver is bonus income, which is rising for higher earners but is still negative for other groups. That creates a narrow spending tailwind at the top without lifting the broader consumer base.

- Payroll growth: 1.4% year over year, signaling steady demand

- Wage divergence: 5.6% vs. 2.0% vs. 1.0%, widest gap in a decade

- Unemployment signal: Benefits growth fell to below 9% year over year

At the same time, 61% of business owners said labor shortages are impacting them, according to the Bank of America 2025 Business Owner Report. Demand may be steady, but finding and keeping workers is still a challenge. For business owners, this means aligning pricing and product mix to where income is growing, managing inventory tightly, and investing in productivity to offset staffing gaps.

March 27, 2026

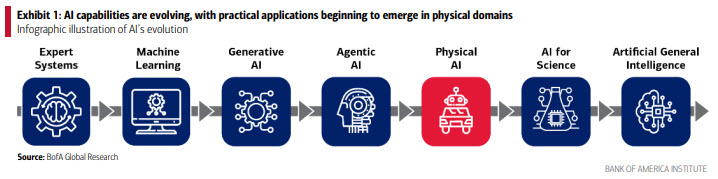

Why physical AI matters for business owners

Physical AI represents a pivotal evolution in artificial intelligence, shifting capability from software into machines that can see, decide, and act in real‑world environments, according to the Bank of America Institute. This transition is creating multi‑trillion‑dollar opportunities for business owners across robotics, autonomous vehicles, and drones.

Breakthroughs in sensors, multimodal foundation models, and simulation now enable robots to learn through interaction instead of rigid rules. These capabilities make them more adaptable and effective in business environments. Early commercial deployments include warehouse automation, manufacturing assistance, logistics workflows, and hazardous‑task handling.

Business owners should pay attention because several forces are accelerating adoption:

- Lower costs and rising capability: Advances in chips, batteries, and AI models are making intelligent machines increasingly affordable for businesses of all sizes.

- Strong investment momentum: Robotics companies received $41 billion in funding in 2025, the highest share of AI equity deals, signaling growing commercial readiness and rapid infrastructure scaling.

- Open‑source innovation: Freely available AI models and tools reduce the need for expensive R&D, allowing companies to customize automation solutions more quickly and cost‑effectively.

As autonomy transitions from rules‑based systems to end‑to‑end, data‑driven intelligence, physical AI is poised to reshape operational models across industries. Early adopters stand to gain efficiency, safety, and productivity advantages that can materially improve competitiveness.

Talk to your specialist about how you might be able to finance these transformative changes for your business.

March 16, 2026

Navigating economic volatility and policy shifts

Business owners are entering a period defined by heightened geopolitical tension and shifting trade policy, both of which have direct implications for planning, cash flow, and long‑term strategy.

With the U.S. and Israel launching a military campaign against Iran on February 28 and retaliatory strikes occurring across the Middle East, business owners are bracing for uncertainty. “While U.S. economic uncertainties and market volatility will likely rise, fiscal and monetary support should keep the U.S. economy clear of recession and corporate profit growth intact,” says Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank.

At the same time, business owners continue to adjust to a shifting trade landscape following the U.S. Supreme Court’s February 20 ruling that struck down tariffs imposed under the International Emergency Economic Powers Act. With questions remaining around tariff refunds and the potential for new trade actions, uncertainty around supply chains, pricing, and procurement strategies is still elevated.

In moments like these, scenario planning becomes an essential discipline. Business owners can strengthen resilience by stress‑testing their assumptions:

- Identify areas where the business is most exposed

- Model potential tariff or cost impacts

- Assess client concentration risks

- Evaluate operational bottlenecks

- Prioritize adaptability over perfect forecasting

“Stress testing your scenarios can equip you to course‑correct fairly quickly, as opposed to saying, ‘This too shall pass.’ It might, but it might not. You’ve got to have the ability to flex when needed,” says Karl Bovee, Business Banking executive for Bank of America.

Together, these strategies can help business owners navigate volatility with clarity and position their organizations for long‑term stability and growth.

February 13, 2026

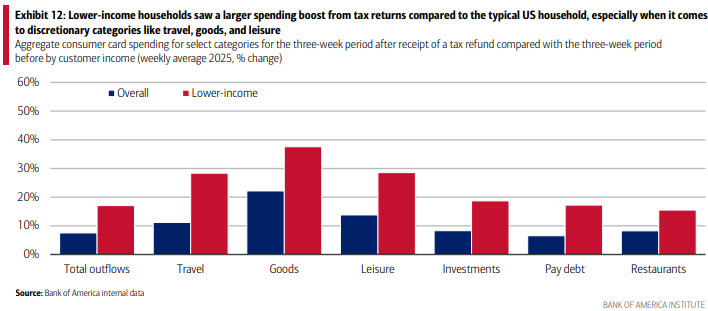

How tax season will affect economic growth

Tax season in 2026 is likely to trigger a meaningful, if temporary, surge in consumer spending, with the biggest impact felt by households that tend to spend a larger share of every additional dollar, according to the Bank of America Institute.

Several forces are lining up behind this boost. Changes under the One Big Beautiful Bill Act, combined with the fact that the IRS did not adjust withholdings last year, are set to deliver larger refunds this spring. Higher standard deductions, new deductions for tip and overtime income, and an increase in the state and local tax deduction cap are all contributing factors.

BofA Global Research estimates that refunds in 2026 could be about $65 billion higher than 2025, a rise of 18%. Most of these payments will be made between February and April.

What might people spend their larger refunds on? Exhibit 12 shows consumer spending trends from 2025 over the three-week period after receipt of a tax refund compared to the prior three weeks. The data shows that largest rise in spending was on goods, but there were also large increases in travel and leisure spending. As expected, given the higher ratio of tax refunds to average monthly spending, the boost was larger for lower-income households.

“The positive wealth effect among higher-income households will likely underpin solid levels of personal consumption expenditures (PCE) this year, as will the expected chunky tax refunds for many households over the first half of 2026,” said Joe Quinlan, head of Market Strategy in the Chief Investment Office at Merrill and Bank of America Private Bank.

November 20, 2025

Insights from the 2025 Business Owner Report

Bank of America’s 2025 Business Owner Report offers a clear look at how small and mid-sized business owners view the year ahead. The primary takeaway is this. Growth is still the focus even as inflation, supply chain pressures and labor shortages create challenges.

According to the report, 74% of business owners expect revenue to increase in the next year and nearly 60% plan to expand their businesses. This is consistent with Bank of America Institute data showing that small business profitability has still been resilient throughout 2025. About half of business owners are hopeful that the local, national and global economies will improve. Their confidence is closely tied to key factors like stabilizing tariff policy, cooling inflation, lower interest rates and stronger supply chains.

Sharon Miller, President and Co-Head of Business Banking at Bank of America, says this sense of cautious optimism is well earned. “Business owners are approaching the coming year with confidence and a clear focus on growth. Many plan to retain their current staff and hire more and anticipate that local, national and global economies will improve.”

The report also sheds light on pressures from a tight labor market. 61% of business owners say they are affected by labor shortages. Many are responding by personally working more hours and raising wages to attract competitive talent. Only 1% are planning layoffs in the next year while 43% expect to hire.

Inflation continues to affect 88% of business owners. As a response, 64% are raising prices and 39% are reevaluating cash flow and spending strategies.

Digital transformation is clearly accelerating. 77% of business owners have already integrated AI into operations including marketing, content creation and customer service. And 91% plan to adopt more digital tools in the next five years. These investments include accepting more digital payments, streamlining workflows and improving cybersecurity.

Read the full report and use real insights from business owners to drive smarter decisions in 2025.

October 27, 2025

Resilient U.S. growth powered by strong wages and AI investment

Business owners must be nimble when there’s a lack of official data, such as during a government shutdown. Bank of America internal data signals that U.S. job growth likely continued to decline. However, wage growth is picking up across income levels, even if high earners are faring better than lower-income households. This combination of higher wages and strong spending is supportive of resilient U.S. growth.

Bank of America data shows that small business profitability, measured by the inflow-to-outflow ratio, has held steady, though slower deposit growth suggests moderating revenues. Alternative hiring indicators fell 7% in September from the 2024 average, with business applications signaling softer job creation. Meanwhile, credit card balances rose 3% as firms carried more debt, but easing lending standards indicate credit access remains resilient.

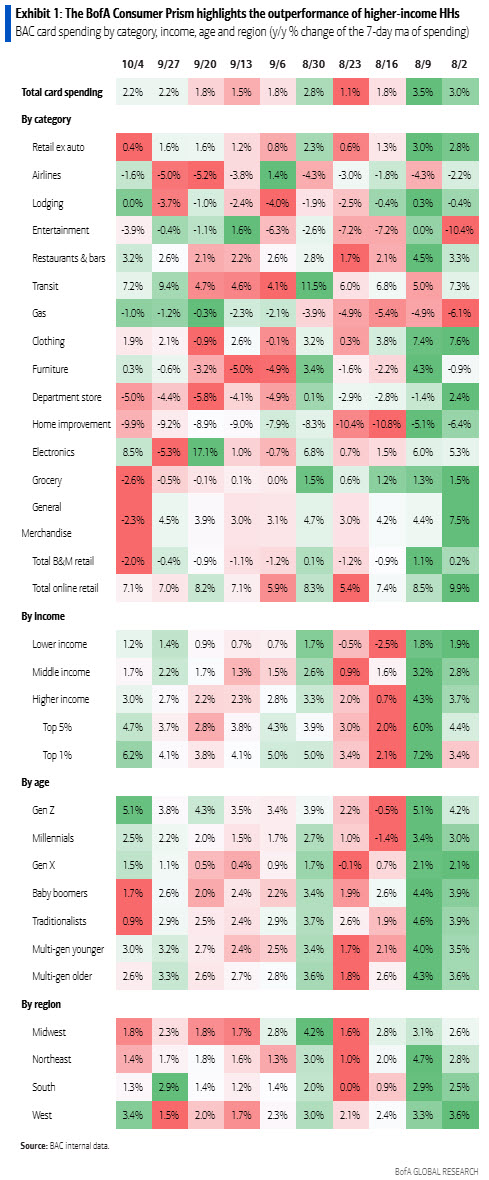

As more people look to alternative data to fill in the gaps, Bank of America created a heatmap, called the Bank of America’s Consumer Prism, using the bank’s total aggregated credit and debit card spending data by category, income, age and region. See Exhibit 1.

Two trends stand out in the BofA Consumer Prism for business owners. First, growth in higher-income spending continues to outpace lower-income spending. The top 5% and top 1% are seeing particularly robust year-over-year spending growth rates. Second, Gen X households have had the weakest spending growth for most of the last quarter. Unlike younger generations, earnings might have peaked for many Gen X-ers, but they potentially haven't accumulated as much equity and real estate wealth as older generations. These insights can help business owners adjust what consumers they target and look for unmet needs in the market.

Where the AI boom fits into the economic data

In Bank of America client talks, one of the most frequently discussed topics is AI and what it means for growth, productivity, and the labor market. The most immediate effect from AI on the economy is the investment, bank analysts say. This should continue to be a boon for growth, though tariff frontloading blurs the picture. Bank analysts do not find evidence of AI usage leading to job losses, especially across white collar occupations. The productivity story seems to be winning, at least so far.

September 29, 2025

From bricks to bytes: Artificial intelligence for business owners

It’s been nearly three years since artificial intelligence (AI) went public. In that time, its promise has grown every quarter across seemingly every sector of the economy. Amid stunning headlines touting Big Tech’s capital mobilization, over $300 billion1 in planned spending in 2025 alone, investors are keen to understand how they could potentially benefit from this revolutionary technology. “We haven’t even scratched the surface about how much money is needed,” says Haim Israel, Head of Global Thematic Research for BofA Global Research.

In the video above, Israel talks to Chris Hyzy, Chief Investment Officer, Merrill and Bank of America Private Bank, about the trajectory of the AI buildout, the race between U.S. and China for dominance, and potential beneficiaries — from commodities, such as copper, nickel and silicon, to sectors including energy and transportation — that may feel an AI boost. Additionally, they discuss the risks associated with AI and what you should keep an eye on as this technology revolution accelerates.

1 Tech megacaps plan to spend more than $300 billion in 2025, Samantha Subin. CNBC, Feb. 8, 2025.

September 8, 2025

Top lessons from the 2025 Workplace Benefits Report

Running a business today means balancing growth with the reality of employee needs. The 2025 Workplace Benefits Report highlights where employees are struggling and what business owners should prioritize in 2025.

What employees want

Employees are under pressure. Eighty-five percent carry personal debt, and more than half have credit card balances. Retirement and emergency savings are still top priorities, yet half haven’t reached their emergency savings goal, often because debt repayment takes precedence. This stress pushes workers to look beyond traditional health insurance and 401(k)s. They want help managing debt, planning retirement income, and building financial skills.

One of the clearest signals in the report is the power of equity. Seventy-one percent of employees say stock awards influenced their decision to accept or stay in a job. Career optimism is also higher for those who receive equity (70% versus 64% without). Yet few small businesses extend equity broadly, leaving a strong retention lever untapped.

Communication is another weak spot. Even when benefits exist, employees often don’t know about them. Only 39% of workers are aware of investment services at work, compared with 52% of employers who say they provide them. Similar gaps appear in mentoring, wellness reimbursements, and emergency loans.

Where small businesses lag

The divide between large and small firms is sharp. Employees at large companies report greater financial well-being (57%) than those at small businesses (41%). Larger employers are more likely to offer financial wellness programs, while 51% of small businesses focus mainly on competitive fees.

Technology is widening the gap. Eight in 10 employers use AI for efficiency and talent management, but nearly a third of small businesses don’t use it at all. Only 21% of small firms say AI improves hiring, compared with 46% of large employers.

The takeaway is simple: benefits strategy is business strategy. In 2025, employees expect equity, savings support, debt solutions, smart use of AI, and clear communication. To explore tailored solutions for your business, consider speaking with a Bank of America relationship manager.

Ready to meet with a specialist?

Our specialists are ready with advice and guidance to help move your business forward.

Ready to meet with a specialist?

Our specialists are ready with advice and guidance to help move your business forward.

Important Disclosures and Information

"Bank of America" and "BofA Securities" are the marketing names used by the Global Banking and Global Markets divisions of Bank of America Corporation. Lending, derivatives, other commercial banking activities, and trading in certain financial instruments are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., Member FDIC. Trading in securities and financial instruments, and strategic advisory, and other investment banking activities, are performed globally by investment banking affiliates of Bank of America Corporation ("Investment Banking Affiliates"), including, in the United States, BofA Securities, Inc., which is a registered broker-dealer and Member of SIPC, and, in other jurisdictions, by locally registered entities. BofA Securities, Inc. is a registered futures commission merchant with the CFTC and a member of the NFA.

“Retirement and Personal Wealth Solutions” is the institutional retirement business of Bank of America Corporation (“BofA Corp.”) operating under the name “Bank of America.” Investment advisory and brokerage services are provided by wholly owned non-bank affiliates of BofA Corp., including Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as "MLPF&S" or "Merrill"), a dually registered broker-dealer and investment adviser and Member SIPC. Banking activities may be performed by wholly owned banking affiliates of BofA Corp., including Bank of America, N.A., Member FDIC.

Investing involves risk, including the possible loss of principal. Past performance is no guarantee of future results.

Investments have varying degrees of risk. Some of the risks involved with equity securities include the possibility that the value of the stocks may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the U.S. or abroad. Bonds are subject to interest rate, inflation and credit risks. Treasury bills are less volatile than longer-term fixed income securities and are guaranteed as to timely payment of principal and interest by the U.S. government. Investments in a certain industry or sector may pose additional risk due to lack of diversification and sector concentration. There are special risks associated with an investment in commodities, including market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes and the impact of adverse political or financial factors.

Diversification does not ensure a profit or protect against loss in declining markets.

Opinions are as of the date of these articles and are subject to change.

This information should not be construed as investment advice and is subject to change. It is provided for informational purposes only and is not intended to be either a specific offer by Bank of America, Merrill or any affiliate to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available.

These materials have been prepared by Bank of America Institute and are provided to you for general information purposes only. To the extent these materials reference Bank of America data, such materials are not intended to be reflective or indicative of, and should not be relied upon as, the results of operations, financial conditions or performance of Bank of America. Bank of America Institute is a think tank dedicated to uncovering powerful insights that move business and society forward. Drawing on data and resources from across the bank and the world, the Institute delivers important, original perspectives on the economy, sustainability and global transformation. Unless otherwise specifically stated, any views or opinions expressed herein are solely those of Bank of America Institute and any individual authors listed, and are not the product of the BofA Global Research department or any other department of Bank of America Corporation or its affiliates and/or subsidiaries (collectively Bank of America). The views in these materials may differ from the views and opinions expressed by the BofA Global Research department or other departments or divisions of Bank of America. Information has been obtained from sources believed to be reliable, but Bank of America does not warrant its completeness or accuracy. Views and estimates constitute our judgment as of the date of these materials and are subject to change without notice. The views expressed herein should not be construed as individual investment advice for any particular person and are not intended as recommendations of particular securities, financial instruments, strategies or banking services for a particular person. This material does not constitute an offer or an invitation by or on behalf of Bank of America to any person to buy or sell any security or financial instrument or engage in any banking service. Nothing in these materials constitutes investment, legal, accounting or tax advice.

Bank of America, Merrill, their affiliates and advisors do not provide legal, tax or accounting advice. Consult your own legal and/or tax advisors before making any financial decisions. Any informational materials provided are for your discussion or review purposes only. The content on the Center for Business Empowerment (including, without limitations, third party and any Bank of America content) is provided “as is” and carries no express or implied warranties, or promise or guaranty of success. Bank of America does not warrant or guarantee the accuracy, reliability, completeness, usefulness, non-infringement of intellectual property rights, or quality of any content, regardless of who originates that content, and disclaims the same to the extent allowable by law. All third party trademarks, service marks, trade names and logos referenced in this material are the property of their respective owners. Bank of America does not deliver and is not responsible for the products, services or performance of any third party.

Not all materials on the Center for Business Empowerment will be available in Spanish.

Certain links may direct you away from Bank of America to unaffiliated sites. Bank of America has not been involved in the preparation of the content supplied at unaffiliated sites and does not guarantee or assume any responsibility for their content. When you visit these sites, you are agreeing to all of their terms of use, including their privacy and security policies.

Credit cards, credit lines and loans are subject to credit approval and creditworthiness. Some restrictions may apply.

Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as “MLPF&S" or “Merrill") makes available certain investment products sponsored, managed, distributed or provided by companies that are affiliates of Bank of America Corporation (“BofA Corp."). MLPF&S is a registered broker-dealer, registered investment adviser, Member SIPC, and a wholly owned subsidiary of BofA Corp.

Banking products are provided by Bank of America, N.A., and affiliated banks, Members FDIC, and wholly owned subsidiaries of BofA Corp.

“Bank of America” and “BofA Securities” are the marketing names used by the Global Banking and Global Markets division of Bank of America Corporation. Lending, derivatives, other commercial banking activities, and trading in certain financial instruments are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., Member FDIC. Trading in securities and financial instruments, and strategic advisory, and other investment banking activities, are performed globally by investment banking affiliates of Bank of America Corporation (“Investment Banking Affiliates”), including, in the United States, BofA Securities, Inc., which is a registered broker-dealer and Member of SIPC, and, in other jurisdictions, by locally registered entities. BofA Securities, Inc. is a registered futures commission merchant with the CFTC and a member of the NFA.

Investment products: