On this page

What do employers need to know about state-sponsored retirement programs?

June 15, 2026 | 4 minute read

Key takeaways

- Increasingly, states are requiring businesses to offer retirement plans to employees

- State-sponsored retirement programs can offer a simple, low-cost way of meeting these requirements

- Employer-sponsored retirement plans are more flexible and full-featured

Workers in the U.S. have long been facing a substantial retirement plan coverage gap. In fact, only about 50% of workers in the private sector participate in an employer-sponsored retirement plan.1 The biggest reason? Their employers simply don’t offer one. To help close this gap, many states have introduced retirement programs, some of which require employers — including sole proprietors and the self-employed — to participate. As these programs expand, business owners have more options than ever. But making the right choice means first understanding how these programs work, what may be required of your business and which alternatives are available.

What is a state-sponsored retirement program?

State-sponsored retirement programs are created by individual states to provide more employees with a way to save for retirement — especially those whose employers don't offer plans. Here’s what you need to know about them:

States set up and run the programs

Each program is established and managed at the state level, making it a simple way for employers to meet that state’s participation requirements.

They’re usually offered by states with a retirement plan participation mandate

Many states require businesses with employees — sometimes including sole proprietors and the self-employed — to offer a retirement plan, either by setting up their own or enrolling in the state program.

Automatic enrollment is the norm

Employees are typically enrolled by default through payroll. However, they can opt out or adjust their contribution amount at any time.

Contributions typically go into a Roth IRA

In many programs, employee contributions are made aſter tax to a Roth IRA. However, the program structure and features will vary by state.

They’re designed to be straightforward

Employers generally have limited administrative responsibilities, such as registering for the program, helping ensure eligible employees are enrolled, processing contributions through payroll and keeping employee information up to date.

Employer contributions are usually not allowed

Most state-sponsored programs don’t allow employers to make matching or other contributions to their employees’ accounts.

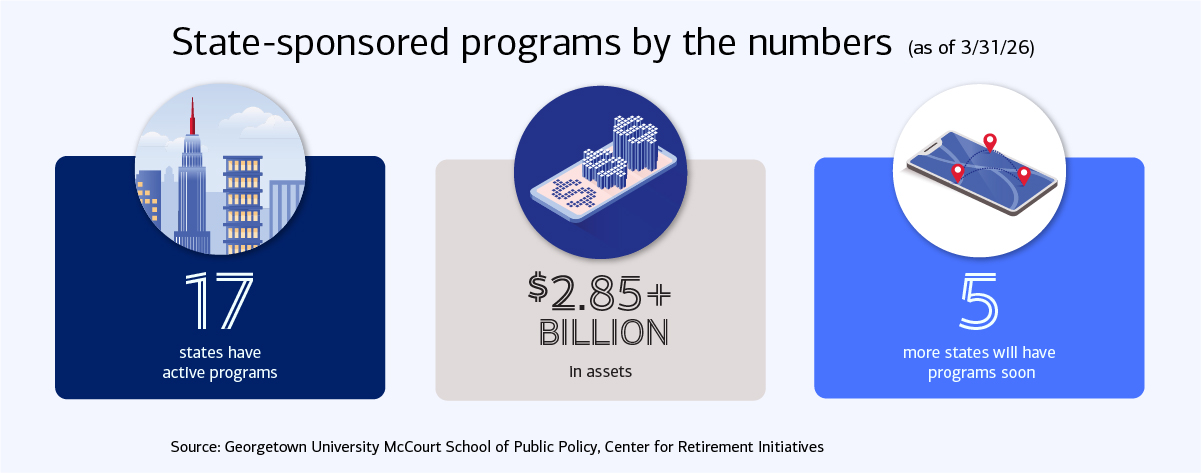

Which states offer retirement programs?

As of April 30, 2026, 22 states have enacted new programs for private sector workers. But nearly every state in the U.S. has at least considered legislation to establish state-facilitated retirement savings programs, so this number is expected to grow.

Learn more about individual state programs with our most recent fact sheet.

State-sponsored programs vs. employer-sponsored plans

While both are designed to facilitate saving for retirement, there are a number of key differences between employer-sponsored plans and state-sponsored programs.

|

Column Header

|

Column Header

Employer-sponsored plan |

Column Header

State-sponsored program |

||

|---|---|---|---|---|

|

Pre/post-tax contributions |

Both options available |

Post-tax only (auto-IRA) |

||

|

Employer match or other contributions |

Optional |

Not allowed |

||

|

Employer tax credits |

Eligible |

Not eligible |

||

|

Investment lineup |

Wide range of funds available |

Limited; Often target date funds |

|

Column 1 Content Row 1

Pre/post-tax contributions |

Column 2 Content Row 1

Both options available |

Column 3 Content Row 1

Post-tax only (auto-IRA) |

|

Column 1 Content Row 2

Employer match or other contributions |

Column 2 Content Row 2

Optional |

Column 3 Content Row 2

Not allowed |

|

Column 1 Content Row 3

Employer tax credits |

Column 2 Content Row 3

Eligible |

Column 3 Content Row 3

Not eligible |

|

Column 1 Content Row 4

Investment lineup |

Column 2 Content Row 4

Wide range of funds available |

Column 3 Content Row 4

Limited; Often target date funds |

What factors should you consider?

State-sponsored retirement programs are designed to offer a simple, accessible path to compliance with minimal effort. However, some employers may prefer employer-sponsored plans, which offer more flexibility and long-term value for their business and employees.

Understanding the differences can help you decide which aligns best with your goals.

Why a state‑sponsored program?

Business owners often choose state programs when they are looking for:

- Low cost — Typically, minimal or no direct employer fees

- Simplicity — Designed to be easy to set up and maintain

- Minimal administration — Limited employer involvement after initial setup

- Straightforward way to meet applicable state requirements

Why an employer-sponsored plan?

As businesses grow, some employers begin to look for features that go beyond basic compliance, such as:

- More savings flexibility — Higher contribution limits and broader participation options

- Additional ways to support employees — The ability to contribute as an employer or offer a more competitive benefit

- Greater investment choice — More options to align with individual preferences and financial goals

- Plan design flexibility — The ability to tailor a program to the needs of the business

- Long‑term scalability — A solution that can evolve as the business grows

- Employer tax advantages — Costs associated with employer contributions and plan expenses are generally deductible from the employer’s income2

Putting it into perspective

For many businesses, state-sponsored programs are a practical way to meet applicable state requirements. For others, they’re a first step before exploring alternatives that offer more flexibility, customization and long-term value. Ultimately, there isn’t a one-size-fits-all answer. But with some careful consideration, you can find the option that best fits where your business is today — and where you want it to go tomorrow.

Bank of America Workplace Benefits™ for small business owners and entrepreneurs

Find out how our experienced team can help you build a benefits plan that truly fits your business's needs.

How do employers choose and set up a workplace retirement plan?

Picking the right plan for your business and getting it off the ground is easier than you might think.

Bank of America Workplace Benefits™ is here to help your business — and your employees — thrive

Find out how our experienced team can help you build a benefits plan that truly fits your business's needs.

Important Disclosures and Information

Bank of America, Merrill, their affiliates and advisors do not provide legal, tax or accounting advice. Consult your own legal and/or tax advisors before making any financial decisions. Any informational materials provided are for your discussion or review purposes only. The content on the Center for Business Empowerment (including, without limitations, third party and any Bank of America content) is provided “as is” and carries no express or implied warranties, or promise or guaranty of success. Bank of America does not warrant or guarantee the accuracy, reliability, completeness, usefulness, non-infringement of intellectual property rights, or quality of any content, regardless of who originates that content, and disclaims the same to the extent allowable by law. All third party trademarks, service marks, trade names and logos referenced in this material are the property of their respective owners. Bank of America does not deliver and is not responsible for the products, services or performance of any third party.

Not all materials on the Center for Business Empowerment will be available in Spanish.

Certain links may direct you away from Bank of America to unaffiliated sites. Bank of America has not been involved in the preparation of the content supplied at unaffiliated sites and does not guarantee or assume any responsibility for their content. When you visit these sites, you are agreeing to all of their terms of use, including their privacy and security policies.

Credit cards, credit lines and loans are subject to credit approval and creditworthiness. Some restrictions may apply.

Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as “MLPF&S” or “Merrill”) makes available certain investment products sponsored, managed, distributed or provided by companies that are affiliates of Bank of America Corporation (“BofA Corp.”). MLPF&S is a registered broker-dealer, registered investment adviser, Member SIPC, and a wholly owned subsidiary of BofA Corp.

Banking products are provided by Bank of America, N.A., and affiliated banks, Members FDIC, and wholly owned subsidiaries of BofA Corp.

“Bank of America” and “BofA Securities” are the marketing names used by the Global Banking and Global Markets division of Bank of America Corporation. Lending, derivatives, other commercial banking activities, and trading in certain financial instruments are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., Member FDIC. Trading in securities and financial instruments, and strategic advisory, and other investment banking activities, are performed globally by investment banking affiliates of Bank of America Corporation (“Investment Banking Affiliates”), including, in the United States, BofA Securities, Inc., which is a registered broker-dealer and Member of SIPC, and, in other jurisdictions, by locally registered entities. BofA Securities, Inc. is a registered futures commission merchant with the CFTC and a member of the NFA.

Investment products: