How can a Pooled Employer Plan (PEP) benefit small to mid-size businesses?

April 9, 2026 | 3 minute read

Key takeaways

- Joining a PEP can help make offering a retirement plan to your employees less complicated and potentially more affordable than with a traditional 401(k).

- With a PEP, multiple employers “pool together” to participate in a plan managed by a Pooled Plan Provider (PPP).

- A PEP effectively outsources most of the legal responsibility and administrative burden to entities outside of your company.

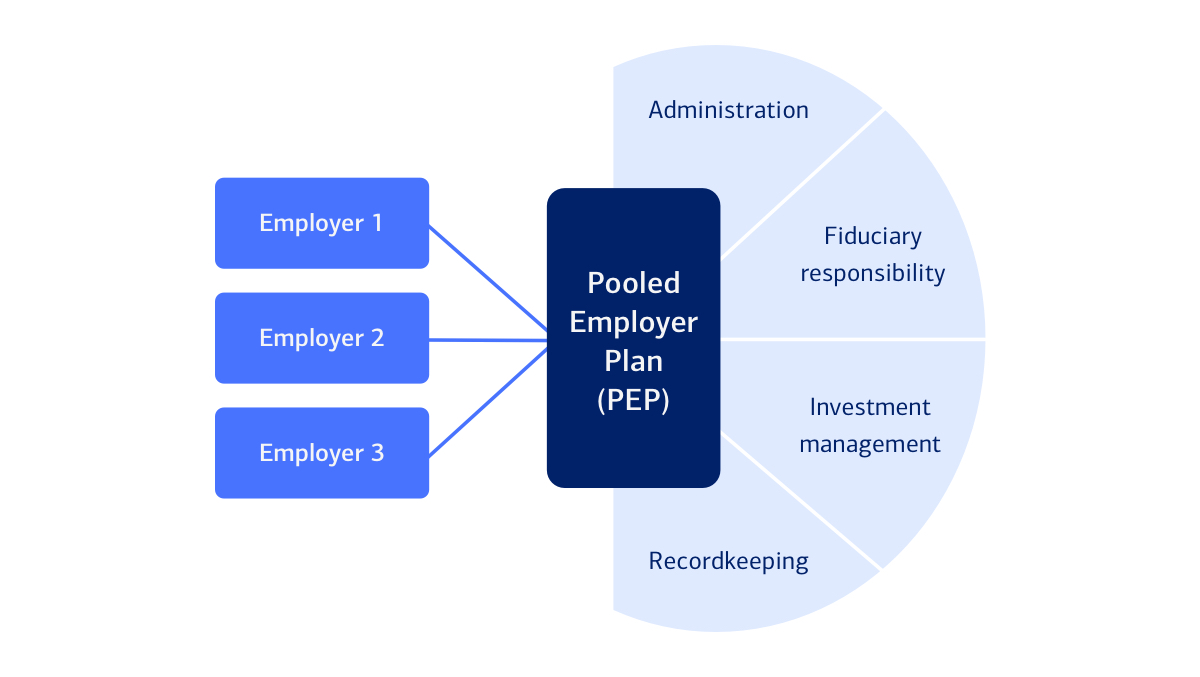

For employers who've been reluctant to offer their employees a 401(k) because of concerns about complexity, regulations or administrative burden, the Pooled Employer Plan, or PEP, has become an increasingly popular option. A PEP is a defined contribution plan that allows employers of different sizes and from different industries to join in one pooled plan instead of sponsoring standalone 401(k) plans. That means individual employers don't have to carry the full responsibility for plan administration and compliance.

PEPs are growing in popularity

The number of participants with balances in PEPs increased 49% from 2023 to 2024.1 And that figure is projected to rise as more and more employers choose this cost-effective, less complex alternative to a traditional 401(k).

The rapidly expanding PEP market2

The benefits of a PEP

A PEP offers significant benefits for businesses that are concerned about the administrative burden. expense and risk of a traditional 401(k).

Time savings: A Pooled Plan Provider (PPP) handles much of the plan administration, while an investment manager takes discretion to select and make periodic changes to the investments in your plan's menu.

Risk reduction: A PEP allows employers to transfer most of the administrative and fiduciary responsibilities of sponsoring a retirement plan to the PPP.

Cost efficiencies: A PEP may introduce cost efficiencies through administrative streamlining and shared audit costs.3

Tax credit opportunities: Startup and contribution credits can help employers reduce costs even more. These include:

How is a PEP managed?

A number of entities all work together to manage a PEP. They greatly reduce the administrative burden to employers, as well as make sure the plan operates smoothly and remains in compliance with regulations.

PPP: The PPP has fiduciary responsibility for the overall management of the plan.

- 3(16) plan administrator: The PPP serves as the 3(16) operational fiduciary and is responsible for the day-to-day administration of the plan including eligibility, beneficiary tracking and plan disbursements. The PPP handles the heavy lifting so you can focus on running your business.

- ERISA 3(38) investment manager: An ERISA 3(38) investment manager takes responsibility for choosing and monitoring the investments offered to participants in the plan, reducing risk and streamlining plan oversight.

- Recordkeeper: The recordkeeper is responsible for holding plan assets, keeping track of participant information and providing an easy-to-use website where employees can view and manage their accounts.

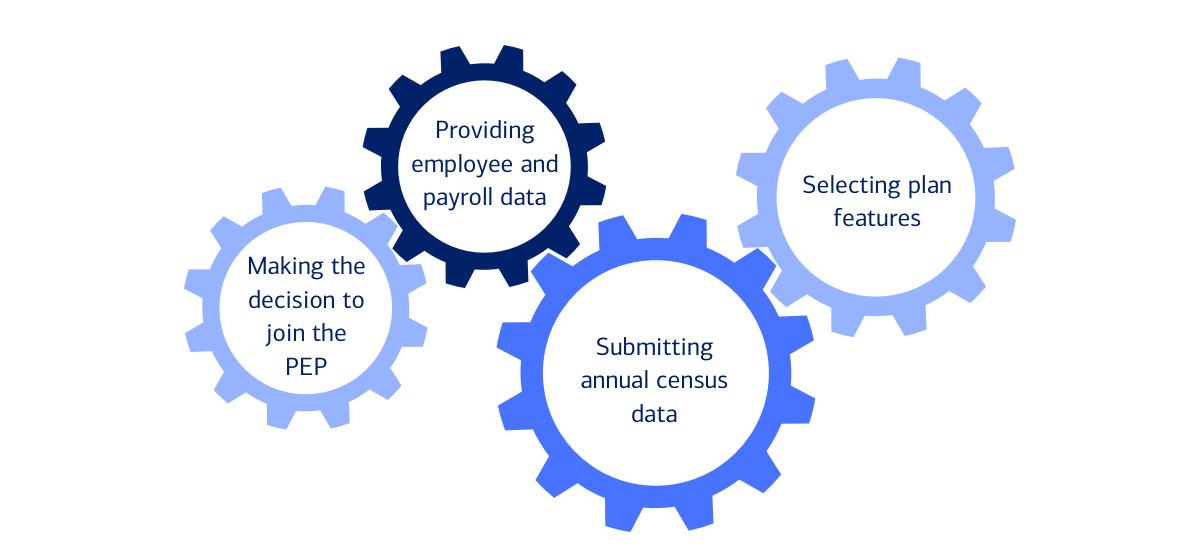

What employers still need to do

Certain responsibilities remain in the hands of employers participating in a PEP. These include:

Is a PEP right for your business?

While businesses of any size can join a PEP, small to mid-size companies that want to sponsor retirement plans for their employees but are concerned about cost, administration and regulatory requirements might find a PEP to be an excellent solution. But it may offer less flexibility and fewer customizable options than standalone plans. However, key plan features — like eligibility, matching and vesting — remain in the employer's control. This can help businesses build a plan that meets their needs while enjoying the benefits that come with a pooled plan.

Questions?

If you'd like more information about PEPs, feel free to reach out to your Bank of America representative. Or find a specialist who can help.

Bank of America Workplace Benefits™ for small business owners and entrepreneurs

Find out how our experienced team can help you build a benefits plan that truly fits your business's needs.

How do employers choose and set up a workplace retirement plan?

Picking the right plan for your business and getting it off the ground is easier than you might think.

Bank of America Workplace Benefits™ is here to help your business — and your employees — thrive

Find out how our experienced team can help you build a benefits plan that truly fits your business's needs.

1 Cerulli Associates, "PEPs and Participant Personalization Fuel Recordkeeper Growth."

2 See note 1, above.

3 Employers should carefully evaluate the fees and expenses associated with any Pooled Employer Plan before onboarding. PEP costs can vary and employers should compare pricing and features against other available retirement plan solutions to determine the best fit for their company.

4 Retirement Plans Startup Costs Tax Credit. For more information, visit the IRS website, irs.gov/retirement-plans/retirement-plans-startup-costs-tax-credit.

Important Disclosures and Information

Bank of America, Merrill, their affiliates and advisors do not provide legal, tax or accounting advice. Consult your own legal and/or tax advisors before making any financial decisions. Any informational materials provided are for your discussion or review purposes only. The content on the Center for Business Empowerment (including, without limitations, third party and any Bank of America content) is provided “as is” and carries no express or implied warranties, or promise or guaranty of success. Bank of America does not warrant or guarantee the accuracy, reliability, completeness, usefulness, non-infringement of intellectual property rights, or quality of any content, regardless of who originates that content, and disclaims the same to the extent allowable by law. All third party trademarks, service marks, trade names and logos referenced in this material are the property of their respective owners. Bank of America does not deliver and is not responsible for the products, services or performance of any third party.

Not all materials on the Center for Business Empowerment will be available in Spanish.

Certain links may direct you away from Bank of America to unaffiliated sites. Bank of America has not been involved in the preparation of the content supplied at unaffiliated sites and does not guarantee or assume any responsibility for their content. When you visit these sites, you are agreeing to all of their terms of use, including their privacy and security policies.

Credit cards, credit lines and loans are subject to credit approval and creditworthiness. Some restrictions may apply.

Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as “MLPF&S” or “Merrill”) makes available certain investment products sponsored, managed, distributed or provided by companies that are affiliates of Bank of America Corporation (“BofA Corp.”). MLPF&S is a registered broker-dealer, registered investment adviser, Member SIPC, and a wholly owned subsidiary of BofA Corp.

Banking products are provided by Bank of America, N.A., and affiliated banks, Members FDIC, and wholly owned subsidiaries of BofA Corp.

“Bank of America” and “BofA Securities” are the marketing names used by the Global Banking and Global Markets division of Bank of America Corporation. Lending, derivatives, other commercial banking activities, and trading in certain financial instruments are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., Member FDIC. Trading in securities and financial instruments, and strategic advisory, and other investment banking activities, are performed globally by investment banking affiliates of Bank of America Corporation (“Investment Banking Affiliates”), including, in the United States, BofA Securities, Inc., which is a registered broker-dealer and Member of SIPC, and, in other jurisdictions, by locally registered entities. BofA Securities, Inc. is a registered futures commission merchant with the CFTC and a member of the NFA.

Investment products: